Financial Independence, Retire Early (FIRE): The Blueprint to Freedom from the 9–5

The idea of waking up without an alarm clock, choosing how to spend your time, and never worrying about money again sounds like a dream. But for a growing number of people around the world, it’s not a fantasy — it’s a plan.

Financial Independence, Retire Early — commonly known as FIRE — is a movement focused on building enough wealth to live off investments rather than a paycheck. While traditional retirement often happens in your 60s, those pursuing FIRE aim to reach financial independence decades earlier.

But what does FIRE really mean? Is it realistic? And how can someone start working toward it today?

Let’s break it down clearly and practically.

What Is Financial Independence?

Financial independence means having enough assets that your investments generate sufficient income to cover your living expenses — indefinitely.

You no longer depend on employment income to survive. Work becomes optional.

This doesn’t necessarily mean never working again. Many people who reach financial independence continue working on passion projects, start businesses, volunteer, or shift to part-time roles. The key difference is choice.

Understanding the FIRE Movement

The modern FIRE movement gained momentum through personal finance blogs and books like Your Money or Your Life by Vicki Robin and Joe Dominguez. Over time, online communities expanded the concept into a structured approach:

- Save aggressively.

- Invest consistently.

- Reduce unnecessary expenses.

- Build assets that generate passive income.

- Reach a point where your investments can support your lifestyle.

The core philosophy is simple: the more you save and invest today, the sooner you buy back your time.

The Math Behind FIRE

At its heart, FIRE is driven by numbers — but the math is straightforward.

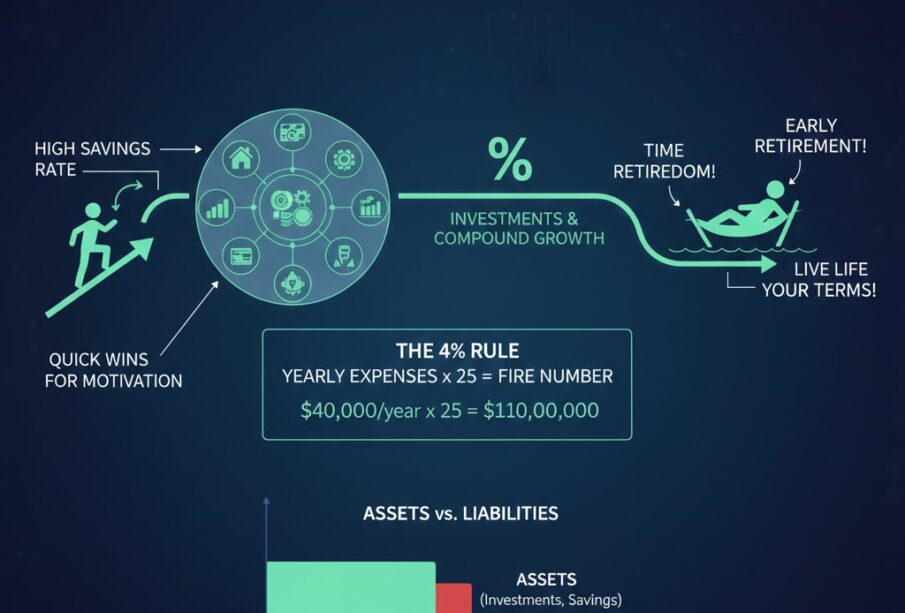

The 25x Rule

A widely used guideline suggests you need approximately 25 times your annual expenses invested to reach financial independence.

Example:

If you spend $40,000 per year, you would need:

$40,000 × 25 = $1,000,000

This rule is based on the 4% withdrawal strategy, which suggests that withdrawing 4% annually from a diversified portfolio has historically supported long-term sustainability.

Why Savings Rate Matters More Than Income

One of the most surprising aspects of FIRE is that how much you save matters more than how much you earn.

- Saving 10% of income could mean 40+ years to independence.

- Saving 50% could reduce that timeline to about 15–20 years.

- Saving 70% could make it possible in under 10–15 years.

Your savings rate directly determines how fast you build freedom.

Types of FIRE

Not everyone pursuing financial independence has the same goal. Over time, several variations have emerged.

1. Lean FIRE

For those willing to live on a minimalist budget. Requires a smaller investment portfolio and lower annual expenses.

2. Fat FIRE

For individuals who want financial independence while maintaining a more comfortable or even luxurious lifestyle. Requires significantly more capital.

3. Coast FIRE

You build enough invested assets early in life that, even if you stop contributing, they will grow to support retirement later. After reaching this point, you only need to earn enough to cover current expenses.

4. Barista FIRE

You reach partial financial independence and take on flexible or part-time work to cover some living costs while investments handle the rest.

Each path reflects different priorities — freedom doesn’t look the same for everyone.

The Core Pillars of FIRE

Achieving financial independence generally rests on four main pillars.

1. High Savings Rate

Aggressive saving is foundational. This often involves:

- Avoiding lifestyle inflation.

- Living below your means.

- Redirecting raises and bonuses into investments.

- Prioritizing needs over impulse purchases.

It’s not about deprivation. It’s about intentional spending.

2. Smart Investing

Savings alone won’t get you to financial independence — investing is essential.

Many in the FIRE community focus on:

- Broad market index funds

- Tax-advantaged retirement accounts

- Real estate investments

- Dividend-producing assets

The goal is steady, long-term growth through diversification and compounding.

3. Expense Awareness

Tracking spending helps identify areas where money leaks away unnoticed. Small recurring expenses often add up more than people expect.

The objective isn’t to eliminate joy — it’s to eliminate waste.

4. Long-Term Discipline

Financial independence doesn’t happen overnight. It requires consistency, especially during market downturns. Emotional investing decisions can delay progress significantly.

The Psychological Side of FIRE

FIRE is as much a mindset shift as a financial strategy.

Delayed Gratification

Choosing long-term freedom over short-term consumption is challenging. Society often promotes spending as a symbol of success. FIRE followers flip that script.

Redefining Success

Instead of bigger houses or luxury cars, success becomes:

- Time autonomy

- Reduced stress

- Personal growth

- Meaningful relationships

Intentional Living

FIRE encourages asking deeper questions:

- What do I truly value?

- How much is enough?

- What would I do if money wasn’t a constraint?

For many, this clarity becomes the most powerful outcome.

Common Criticisms of FIRE

No financial strategy is without debate. FIRE has its critics.

“It’s Only for High Earners”

While higher income accelerates progress, FIRE is more about savings rate than salary. Moderate earners who control expenses and invest consistently can still achieve independence — it may simply take longer.

“It Requires Extreme Frugality”

Some versions of FIRE emphasize minimalism, but not all paths require extreme sacrifices. The movement is flexible. It adapts to personal values.

“Markets Aren’t Guaranteed”

Investment returns vary. That’s why diversification, conservative withdrawal strategies, and flexibility matter. Many who pursue FIRE also build multiple income streams to reduce risk.

Steps to Start Your FIRE Journey

If financial independence appeals to you, here’s how to begin.

1. Calculate Your Annual Expenses

Track spending for several months. Know your baseline number. This is your starting point.

2. Determine Your FI Number

Multiply annual expenses by 25. That gives you a rough target.

3. Increase Your Savings Rate

Look at your largest expenses first:

- Housing

- Transportation

- Food

- Insurance

Small optimizations here can create major gains.

4. Automate Investments

Consistency beats timing the market. Automatic contributions remove emotion from the equation.

5. Avoid Lifestyle Inflation

When income rises, keep expenses stable. Direct extra income toward investments instead of upgraded consumption.

The Role of Compound Growth

Compounding is the engine behind financial independence.

Money invested early grows exponentially over time. A dollar invested in your 20s is significantly more powerful than one invested in your 40s.

Time in the market matters more than timing the market.

Life After FIRE

Reaching financial independence isn’t the end — it’s a transition.

Many people discover that purpose still matters deeply. Common post-FIRE paths include:

- Entrepreneurship

- Creative projects

- Teaching or mentoring

- Travel

- Community involvement

The freedom to choose becomes the real reward.

Is FIRE Right for You?

FIRE isn’t a one-size-fits-all solution. It requires:

- Long-term discipline

- Comfort with delayed gratification

- Consistent investing

- A clear understanding of personal priorities

But even if early retirement isn’t your goal, the principles of FIRE — saving intentionally, investing wisely, and valuing time — can dramatically improve financial security.

You don’t have to retire at 40 to benefit from the mindset.

Final Thoughts

Financial Independence, Retire Early is not about escaping work. It’s about escaping dependency.

It’s about creating a life where money supports your values rather than controlling your choices.

Whether your version of freedom means retiring early, working part-time, or simply reducing financial stress, the core idea remains powerful:

Spend intentionally. Save aggressively. Invest consistently. Value your time.

Because in the end, financial independence isn’t about having millions — it’s about having options.

-

Current vs. Savings Accounts: Why Your Business Needs the Switch

If you are serious about your business — whether small, medium, or ...