Smart Money Management Plan for a Person Earning ₹60,000 Per Month – Simple Budgeting Guide for Financial Stability

Managing money wisely is more important today than ever before. With rising expenses, lifestyle demands, medical costs, rent, loans, and family responsibilities, simply earning ₹60,000 per month is not enough — planning how to use that income matters the most. Many salaried individuals struggle financially not because they earn less, but because they do not manage their money properly.

This article is written specifically for a person earning ₹60,000 per month in India. It explains in a simple way how to budget, save, invest, and secure your future without stress. This is not a complicated financial theory — this is a practical plan that anyone can follow in real life.

Understanding Your Monthly Income

If your take-home salary is ₹60,000 per month, you fall into the middle-income category. You likely have responsibilities such as:

- House rent or EMI

- Food expenses

- Transportation

- Electricity and internet bills

- Family support

- Medical needs

- Personal lifestyle

Without a proper plan, money disappears quickly, and by the end of the month, you may feel stressed or broke.

The first step to financial control is understanding where your money goes.

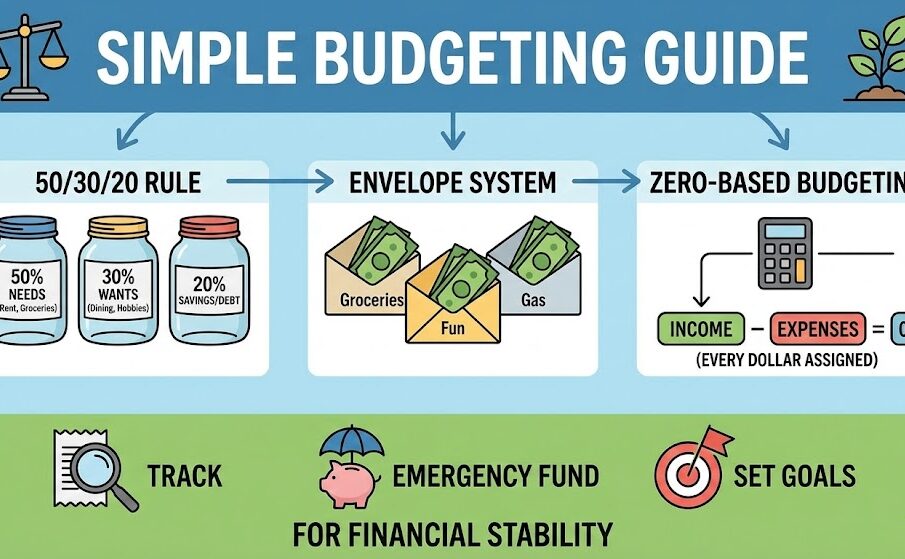

Step 1 – Follow the 50-30-20 Rule

A simple and effective budgeting method is the 50-30-20 rule.

From ₹60,000:

50% for Needs – ₹30,000

This includes:

- Rent or EMI

- Groceries

- Electricity and water bills

- Internet and phone

- Transport (fuel, bus, metro, etc.)

- Basic household expenses

If your rent or EMI is very high, you may need to adjust other expenses slightly.

30% for Wants – ₹18,000

This includes:

- Dining out

- Shopping

- Movies

- Travel

- Personal hobbies

- Gifts

- Extra comfort items

This part should be enjoyed, but kept under control.

20% for Savings & Investment – ₹12,000

This is the most important part of your budget.

You should divide this ₹12,000 as:

- ₹5,000 – Emergency Fund

- ₹5,000 – SIP in Mutual Funds

- ₹2,000 – Personal Savings or Future Goals

This builds long-term financial security.

Step 2 – Build an Emergency Fund

Life is unpredictable. You may face:

- Job loss

- Medical emergency

- Family crisis

- Accident

- Unexpected expenses

You should save at least 6 months of your salary in an emergency fund.

For ₹60,000 salary:

6 months × ₹60,000 = ₹3,60,000

Start slowly:

- Save ₹5,000 per month

- In 5–6 years, you will build a strong safety net

Keep this money in a savings account or fixed deposit.

Step 3 – Start SIP in Mutual Funds

If you want your money to grow, saving alone is not enough. You must invest.

From your ₹12,000 savings portion, invest ₹5,000 in SIP every month.

Good options:

- Nifty 50 Index Fund

- Sensex Index Fund

- Large Cap Mutual Fund

- Balanced Fund

Over time, this can grow into a significant amount due to compounding.

Example:

If you invest ₹5,000 per month for 20 years with average 10% return, you may accumulate several lakhs — much more than simple savings.

Step 4 – Manage Your Rent or EMI Smartly

Ideally, your rent or EMI should not be more than 30% of your income.

For ₹60,000 salary:

- Maximum rent/EMI should be around ₹18,000

If you are paying more than this, try:

- Sharing accommodation

- Moving to a slightly cheaper area

- Reducing other expenses

This prevents financial pressure.

Step 5 – Control Food and Grocery Expenses

Many people overspend on food.

A reasonable monthly food budget for a single person should be:

- ₹6,000 to ₹10,000

For a small family:

- ₹10,000 to ₹15,000

Tips to save:

- Cook at home more

- Avoid frequent ordering

- Buy groceries in bulk

- Plan meals in advance

This alone can save you ₹3,000–₹5,000 per month.

Step 6 – Reduce Unnecessary Expenses

Small expenses add up quickly.

Avoid or reduce:

- Daily coffee from outside

- Too many online orders

- Unnecessary subscriptions

- Expensive gadgets you don’t need

- Frequent cab rides

Even saving ₹2,000–₹3,000 per month makes a big difference over a year.

Step 7 – Get Health Insurance

Medical expenses in India can be very high.

With ₹60,000 salary, you should have:

- Health insurance of at least ₹5–10 lakh

This protects your savings in case of hospital emergency.

Many employers provide insurance, but having your own policy is safer.

Step 8 – Plan for Retirement (EPF / NPS)

If your company provides EPF, that is great.

You can also invest in:

- NPS (National Pension Scheme)

- Additional mutual funds

Even ₹2,000 per month in retirement savings can help you a lot later.

Step 9 – Avoid Too Much Debt

Loans can destroy your financial peace.

Avoid:

- Too many credit cards

- Personal loans for lifestyle

- Buying expensive gadgets on EMI

Only take loans for:

- Education

- Home

- Business

- Medical emergency

Use credit cards responsibly and pay full bill every month.

Step 10 – Set Financial Goals

Your goals may include:

- Buying a house

- Buying a car

- Marriage

- Child education

- Travel

- Higher studies

Break them into short-term and long-term goals and save accordingly.

Example:

- Short-term goal: ₹2 lakh in 2 years

- Long-term goal: ₹20 lakh in 10 years

SIP helps you achieve this.

Sample Monthly Budget for ₹60,000 Salary

Here is a simple example budget:

| Expense | Amount |

|---|---|

| Rent / EMI | ₹18,000 |

| Food & groceries | ₹12,000 |

| Electricity & internet | ₹3,000 |

| Transport | ₹3,000 |

| Personal expenses | ₹6,000 |

| Entertainment | ₹6,000 |

| Savings & investment | ₹12,000 |

| Total | ₹60,000 |

You can adjust this based on your lifestyle.

Step 11 – Side Income (Optional but Powerful)

If possible, try earning extra:

- Freelancing

- Online teaching

- YouTube channel

- Blogging

- Part-time work

Even ₹5,000 extra per month can speed up your financial growth.

Step 12 – Track Your Expenses

Use apps like:

- Money Manager

- Walnut

- Google Sheets

Write down every expense. This gives you full control over your money.

Common Money Mistakes to Avoid

- Not saving anything

- Spending before saving

- Relying only on salary

- No emergency fund

- Too many EMIs

- No investment

- Ignoring insurance

Avoid these, and you will be financially strong.

Final Thoughts

Earning ₹60,000 per month is a good income, but without proper planning, it may never feel enough. By following a simple budgeting plan, saving regularly, investing wisely, and avoiding unnecessary debt, you can build financial stability, peace of mind, and long-term wealth.

Money management is not about earning more — it is about using what you earn in the right way.

-

Demystifying Index Funds and ETFs: A Complete Beginner-to-Advanced Guide for Smart Investors

Yet despite their popularity, many people still feel confused about what index ...